Client Login

Client LoginEquity ISA

An Equity ISA (sometimes referred to as a Stocks and Shares ISA) provides a tax-efficient way to invest in a wide range of assets, normally stock market related, with the potential for higher returns than cash.

Equity ISAs are more of a long-term commitment than a Cash ISA, so they may be a better idea if you are saving for an event a number of years away, such as retirement, university fees for your child/grandchild or something more indulgent.

Please keep in mind that with the prospect of higher returns comes some fluctuation in the value of your investments. At times they may even be lower than when you invested.

However, over the long-term equity based investments are proven to out-perform all other asset types.

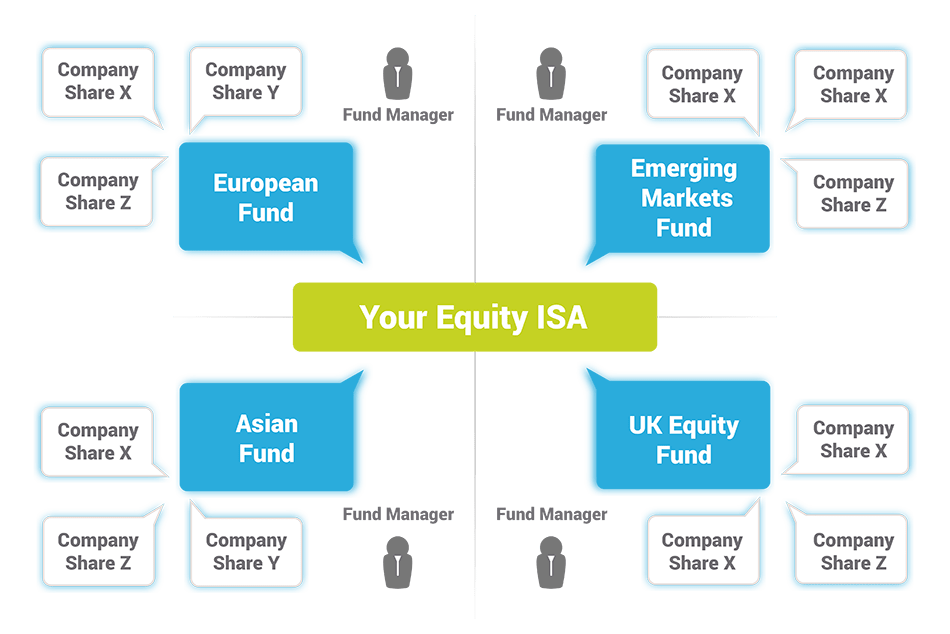

The majority of Equity ISAs use collective investment funds, such as Unit Trusts or Open Ended Investment Companies (OEICs), rather than shares in individual  companies.

companies.

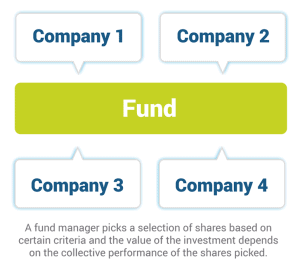

Funds pool investor’s money and appoint an expert (fund manager) to run it. The manager, along with a team of researchers and analysts, look for companies and assets to invest the pool of money in. The companies and assets invested in depend upon the funds aims and objectives. Our guide to funds will give you more information about how they work and the different types available.

Before choosing to invest in a fund, or funds, think about the following; will it help you achieve your investment goals? Are you happy with the level of risk and the investments the manager makes?

The overall value of your ISA is dependent on the value of the funds you hold within it. If you have chosen a fund that pays income, you have the option to take this income as a payment to yourself or reinvest it into your ISA. This does not affect your ISA allowance.

Aside from the tax benefits both Cash and Equity ISAs share, there are specific benefits to investing into an Equity ISA.

Equity-based investments have generated greater returns than Cash over the medium to long-term. However, when choosing your funds, please remember that past performance is just that, and should not be the sole reason to invest.

The benefits of using funds

An alternative to cash – Continuing low interest rates on cash savings and high inflation are a source of frustration of the majority of UK savers. Investing in funds is proven to provide greater returns than cash over the long-term, and although higher risk than cash, they represent less risk than investing directly into company shares yourself.

Diversification

Funds invest in a wide range of assets, such as shares, bonds, property and even gold. They also invest in different markets from the UK to as far afield as China. This diversification reduces the risk of reliance on one asset or market.

Expertise

Funds are run by investment experts (fund managers), who are supported by a team of analysts. They run the fund with the aim of achieving long-term goals. To do this, the fund manager, and their team, analyse the economic environment, individual companies who they either have made, or intend to make investments in to, and the relative performance of different asset classes.

Income or growth

Different funds provide different solutions to match your goals. Some funds have the aim of providing capital growth (referred to as accumulation funds). These are particularly relevant if you are trying to build up the value of your investments over a number of years. Other funds have the aim of providing you with a regular income (referred to as income funds). If you are investing to supplement your other income, perhaps a pension, these funds can be useful. Some funds even offer both.

Simplicity

The days of seeing a financial adviser, or making the trip to your bank or building society in order to invest are long-gone for many people, as are the costs involved. Funds remove a large proportion of the complexity of investing, largely because there is a fund manager in charge of the day to day running of the money you have invested. All you have to do is choose the fund that you feel is right for you. Fund investing is popular for beginners and seasoned investors alike, because of this simplicity.

Convenience

Fund prices don’t move as often as share and asset prices, so there is no need for you to constantly monitor market movements every hour of the day. However, monitoring the performance of the funds in your ISA is all part of the experience, and so you can now get access to fund research and the value of your investments online, whenever you like.

Liquidity

Although investing in cash arguably gives you the quickest and easiest solution if you need access to your money, most funds can be sold at relatively short notice. However, investing should really be for those who can afford to keep their money invested for the long-term as this provides the best scenario for growth.

The benefits of investing through TQ Invest

Choice

We offer a range of choices and options to help find the fund that is right for you. There are literally 1,000s of funds for you to choose from, and you will find information and research on these funds within this website. Simply start searching. For those who prefer to search from a smaller list of funds we have the Hero Funds list, which is a list of the funds our investments experts believe are amongst the best in their field.

Help & Support

You will find a range of useful fund research tools and information within this website. However, if you feel the need to speak to a real person, we have a UK-based helpdesk on hand to answer any questions you have.

Ease of Investing

We provide three routes for you to invest in your ISA. If you prefer to invest online, you can. If you would like someone to invest for you, you can call a member of the team on 0800 294 7221. And if you prefer the traditional way, you can invest by post with a cheque and application form.

A fund is a form of collective investment that allows you to invest in a wide range of assets, including company shares. They are a useful way to access investments you couldn’t manage on your own.

The term collective investment refers to the fact that your money is pooled together with that of other investors and invested on your behalf by the fund manager. This approach gives you access to buying power you wouldn’t be able to achieve on your own.

The fund manager, along with a team of researchers and analysts, runs the fund according to its aims and objectives on a daily basis, monitoring a wide range of factors, including the economy, and the performance of assets and companies.

Types of fund

Unit Trusts

When you invest in a Unit Trust, your money buys ‘units’. The units vary in value according to how well (or not) the Unit Trust’s investments are doing plus whether you take an income or not. So the worth of your investment is mainly determined by the number and the value of the units you own. All Unit Trust funds are ‘open-ended’ which means they can issue new units in response to demand from investors. Unit Trusts trade at their net asset value – that is the value of the investments held by the Unit Trust divided by the number of units issued. Unit Trusts traditionally quote two prices: the buying/offer price and the selling/bid price. The buying/offer price is the price the units are sold to the investor; the selling/bid price (usually 5% lower than the buying price) is the price the investor will get when the units are sold. The difference between the two is known as the bid/offer spread. The price of the Unit Trust is calculated daily, usually at midday. As well as an initial charge of around 5%, unit trusts also levy an annual management charge, which is typically 1.5% per year and is deducted from the fund itself.

OEICs

OEICs are another type of investment fund and many unit trusts are converting to OEICs. An OEIC is a company whose business it is to manage an investment fund. The investor takes a stake in the fund by buying the shares of the OEIC (units) which in common with a unit trust is open-ended. Unlike a unit trust, a single price is quoted for buying and selling the shares. An initial charge – typically 5% of the initial investment’s value – may be deducted from the investment fund plus an exit charge may be applied when you finally withdraw your money. Annual management charges are taken from the amount you have invested in the OEIC.

With a fund your money is invested in a range of assets and individual, reducing the risk associated with holding just one of them yourself.

Fund criteria

Every fund has an objective it aims to achieve for investors. The underlying investments the fund manager makes will depend upon that objective. Broadly, funds make their investments with the following criteria:

- Geography – e.g. UK, America and developing economies such as China

- Asset type – e.g. company shares, corporate and government bonds and commodities

- Company size – e.g. investing in small to medium sized business or large multi-nationals

- Focus – e.g. invest in any type of asset or industry or specialise in a particular one, such as bonds

The criteria the fund follows will determine the risk factor. For instance, if a fund invests primarily in government bonds, then the risk factor is relatively low. Whereas if a fund invests in gold mining companies based in Africa, the risk factor is relatively high.

The majority of funds you can buy take an active approach to management, where the fund manager is constantly looking at the performance of the fund and investment opportunities. However, there are funds that are classed as Passive. These funds are not actively managed, but instead look to track a particular index, such as the FTSE 100.

Fund Charges

The majority of funds have different charges associated with them for the service they are offering to you:

- Initial charge – is the cost of the making the investment in the first instance. The initial charge includes commission the fund provider would pay to a financial adviser, plus an additional amount to cover their administration costs.

- Annual Management Charge (AMC) – is the cost of running the fund on an annual basis and is usually in the region of 0.75% to 1.5%. It includes the remuneration of the manager and his team, plus a proportion that is given to the company that arranged your investments to pay for the service they provide to you.

- Other charges – some funds make additional charges to those mentioned above, such as a performance fee. The type and size of the charge differs greatly between funds, so they can be hard to compare. A great way to compare a fund’s overall charges is to look at its Ongoing Charges Figure (OCF), which calculates every charge as a percentage. The OCF can be found on the fund’s factsheet.

It could be right for you if:

- You have a medium to long-term view on your savings

- You are happy to take a degree of risk in search of greater returns

- You are saving for retirement & want investments to supplement your pension income

It might not be right for you if:

- You have a short-term view on your savings

- You want to take the least amount of risk with your money

- You are aware that interest paid on cash savings may not always keep up with inflation

How much can I invest?

From 6th April 2021, you can invest up to £20,00 in total, with any combination invested in either an Equity ISA or a Cash ISA.

Remember… Tax Advantages

- The gains you make on your ISA are not liable for Capital Gains Tax (CGT)

- You don’t pay Income Tax on any income generated from your ISAs

- You don’t have to declare your ISAs on a self assessment tax return

If I invest a small amount now, can I top up my ISA later?

Answer: Yes, if you have not used your full ISA allowance you are able to top it up during the same tax year. If you wait until after the end of the tax year on 5th April, any further contributions will count towards a new ISA in the new tax year.

MYTH: Investing costs a lot of money

Truth: Using a discount broker, like TQ Invest, reduces the cost of investing in an ISA, to a point where there are no initial charges or commission to pay.